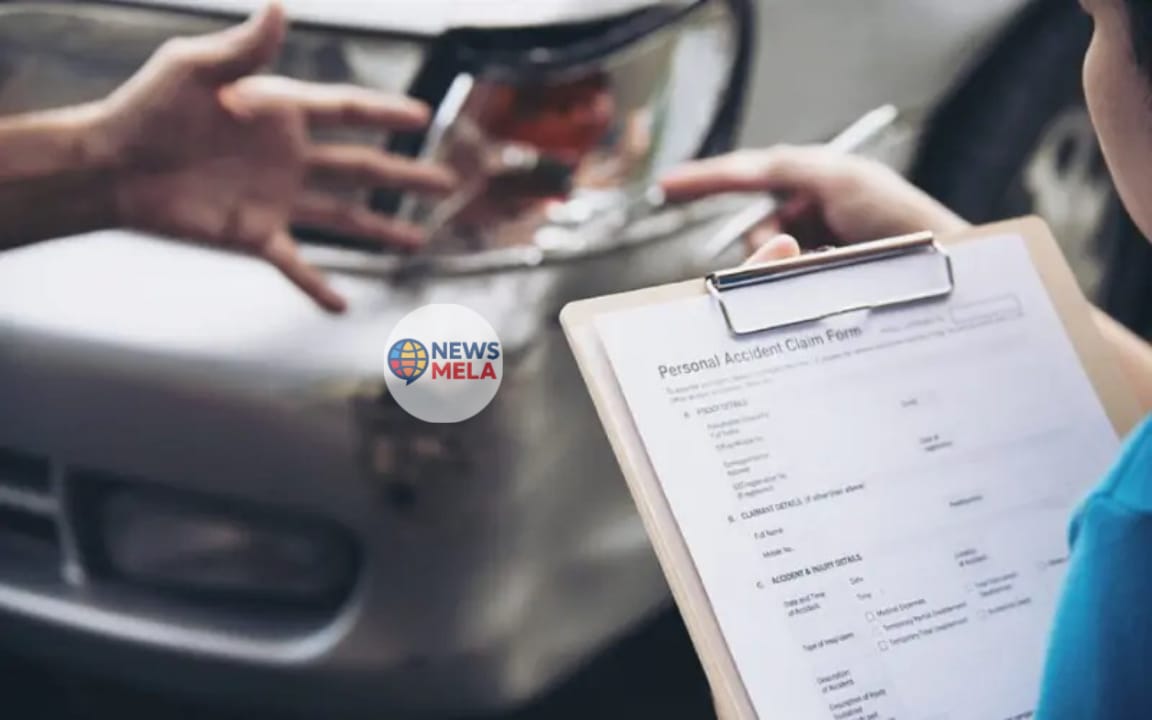

Car insurance is more than just a legal requirement—it is your financial safety net in case of accidents, theft, or damage to your vehicle. While paying insurance premiums may sometimes feel like a burden, the true value of an insurance policy becomes clear the moment you need to file a claim.

Filing a car insurance claim can seem overwhelming, especially if you are dealing with the stress of an accident or sudden car damage. However, if you understand the process well, you can handle it smoothly and ensure that you get the compensation you deserve.

This guide will walk you through everything you need to know about filing a car insurance claim—from what to do immediately after an accident, the documents required, the step-by-step claim process, common mistakes to avoid, and tips to maximize your chances of a hassle-free settlement.

What Is a Car Insurance Claim?

A car insurance claim is a formal request you make to your insurance company, asking them to compensate you for losses or damages covered under your policy. Depending on the situation, a claim may cover:

- Repair costs for your damaged vehicle.

- Third-party damages, including injury or property damage caused to someone else.

- Medical expenses related to injuries from the accident.

- Theft of the vehicle or its parts.

When you file a claim, the insurer will investigate the incident, verify documents, and then either approve or reject your claim based on policy terms.

Types of Car Insurance Claims

Before filing, you should know the types of claims you can make:

1. Cashless Claim

- If your car is repaired at a network garage (partnered with your insurer), you don’t have to pay upfront.

- The insurance company settles the repair bill directly with the garage.

- You only pay for things not covered by your policy, like consumables or deductibles.

2. Reimbursement Claim

- If you get your car repaired at a non-network garage, you pay the bill first.

- After submitting bills and documents, the insurer reimburses the eligible amount.

When Should You File a Car Insurance Claim?

Filing a claim is not always necessary for minor scratches or dents, especially if repair costs are lower than your deductible. However, you should file a claim in the following cases:

- Major accidents with significant vehicle damage.

- Accidents causing injury or death (to yourself, passengers, or third parties).

- Third-party property damage (such as hitting another vehicle, wall, or lamppost).

- Vehicle theft or vandalism.

- Natural disasters (flood, storm, earthquake) or man-made disasters (riots, fire).

Step-by-Step Process to File a Car Insurance Claim

Here is a detailed breakdown of how to file a claim effectively:

Step 1: Ensure Safety First

- Move to a safe spot if possible.

- Check yourself, passengers, and others involved for injuries.

- Call emergency services (police, ambulance) if needed.

Step 2: Inform the Police

- Mandatory in case of accidents involving third parties, injuries, death, theft, or major damage.

- File a First Information Report (FIR)—this is crucial for third-party and theft claims.

- Keep a copy of the FIR as it will be required during the claim process.

Step 3: Inform Your Insurance Company

- Call your insurance company’s toll-free number or use their mobile app/website.

- Inform them about the accident as soon as possible (usually within 24–48 hours).

- Provide details like policy number, date/time of accident, location, and a brief description of the incident.

Step 4: Collect Evidence

- Take clear photos and videos of:

- Damaged vehicle from multiple angles.

- Third-party property damage.

- Injuries (if any).

- Accident location (skid marks, traffic signals, road conditions).

- Gather witness details if possible.

- These will help during claim verification.

Step 5: Submit Required Documents

The documents you typically need include:

- Copy of insurance policy.

- Copy of driving license.

- Vehicle registration certificate (RC).

- Police FIR (for theft or third-party claims).

- Duly filled claim form (online or offline).

- Repair bills (in case of reimbursement).

- Any additional documents requested by the insurer.

Step 6: Vehicle Inspection

- Your insurer will assign a surveyor to assess the damage.

- The surveyor will inspect your vehicle, take photos, and prepare a report.

- Based on this report, the insurer will approve or reject the claim.

Step 7: Vehicle Repair

- If it’s a cashless claim, take your car to a network garage.

- If it’s a reimbursement claim, get the car repaired at any garage and keep all original bills.

Step 8: Claim Settlement

- Once approved, the insurer either:

- Pays the garage directly (cashless).

- Reimburses you after verifying repair bills (reimbursement).

Car Theft Claim Process

If your car is stolen, the process is slightly different:

- File an FIR immediately.

- Inform your insurer about the theft.

- Submit documents like RC, FIR copy, claim form, and original car keys.

- Police will issue a “non-traceable certificate” if the car is not found.

- The insurer will settle the claim by paying the Insured Declared Value (IDV) of your car.

Common Mistakes to Avoid When Filing a Claim

- Delaying claim intimation – Always inform your insurer immediately.

- Repairing before survey – Don’t start repairs until the surveyor inspects the vehicle.

- Hiding facts – Never give false information; insurers can reject fraudulent claims.

- Driving without valid license/RC – Claims will be rejected if the driver lacks documents.

- Not renewing policy on time – Expired policies cannot be claimed.

- Ignoring policy exclusions – Understand what is not covered (e.g., drunk driving, negligence).

Tips for a Smooth Claim Process

- Always keep your insurance documents and emergency numbers handy.

- Install a dashcam—it provides strong accident evidence.

- Maintain regular service records of your car.

- Choose cashless settlement if possible—it’s faster and hassle-free.

- Read your policy terms carefully before filing a claim.

Frequently Asked Questions (FAQs)

Q1. How long does it take to settle a car insurance claim?

It depends on the insurer, but cashless claims usually take a few days, while reimbursement claims may take 1–3 weeks.

Q2. Will filing a claim affect my No-Claim Bonus (NCB)?

Yes, filing a claim will usually reduce or reset your NCB unless it’s for minor windshield/glass damage (depending on insurer).

Q3. Can I file a claim if someone else was driving my car?

Yes, provided the driver had a valid license and your policy covers “any authorized driver.”

Q4. What if the accident was my fault?

If you have a comprehensive policy, your damages will be covered along with third-party liabilities.

Q5. What if my claim is rejected?

You can appeal with the insurer’s grievance redressal team or approach the Insurance Ombudsman.

Conclusion

Filing a car insurance claim may feel intimidating at first, but when broken down into simple steps, the process becomes much easier. The key is to act quickly, stay honest, and keep proper documentation. Whether it’s a minor fender-bender or a major accident, knowing how to handle the situation ensures that you get the rightful compensation without unnecessary stress.

Insurance is your shield against unexpected financial burdens. By understanding the claim process thoroughly, you not only save time and effort but also protect your peace of mind on the road.

Leave a Reply